I distinctly remember a work friend asking me one evening after dinner in Los Angeles, “What are you saving all your money for?” I was stumped and struggled to say something coherent. He knew I lived in a cheap, crappy studio apartment, didn’t really buy much, and didn’t really spend much. Sadly, it has taken me years to know how I should have best answered that question.

Being rich is having money; being wealthy is having time — Margaret Bonnano

I’m a late bloomer when it comes to money. On the one hand, I’ve always had an interest in money but I was never properly educated about personal finance. After graduating college and starting a job as an engineer, I read up on money in books and online, put some money in the stock market, and even attended a seminar on factoring (if you know what that is). I read “Rich Dad Poor Dad.” So it might seem like I was more sophisticated than most. On the other hand, I still didn’t really know what to do other than invest some money in my company’s 401k and some in the stock market. And I still had a lot of anxiety about money and my future. I would have benefited from some guidance from someone who understood money.

Yet I was in a fortunate enough situation after college to be able to wonder and think about these issues. I was very aware that others were living paycheck to paycheck and under less ideal circumstances.

Fast forward to today… the times have certainly changed for many who have recently graduated from college. I see in my own life and in the life of others too much randomness in how people learn about money, save for the future, and make money decisions. Foundational money decisions have to be made all the time from the simple to the complex. How much money should I save? What health insurance plan should I choose? Should I buy or lease a car? Is it better to rent or buy a home? Should I pay off debt or invest my money? How much money should I put into retirement accounts? Is a Roth IRA better than a traditional IRA? How should I invest in real estate? What is infinite banking and is it a scam?

There is no shortage of information out there. There are fintech companies focused on personal finance and money: NerdWallet, Intuit’s Mint, Personal Capital, Wealthfront, Betterment, YNAB, Microsoft Money, LendingHome, Opendoor, Robinhood, Coinbase, etc. Some tech companies are focused on a finance vertical such as Policygenius for insurance or BiggerPockets for real estate investors. There are established old school financial institutions such as Fidelity, Vanguard, Charles Schwab, Goldman Sachs, and all the usual banks such as Bank of America. And there are media companies and websites delivering financial information to consumers such as CNBC, MarketWatch, Bloomberg, MotleyFool, and SeekingAlpha.

And yet… turn to anyone you know and ask them how they learned about personal finance, what they are doing to become financially more secure, or how they are enabling or have enabled their retirement and you’ll realize how haphazard and diverse everyone’s experiences are.

The FIRE movement caught on for many in the last 10 years. Yet at the same time, most American workers aren’t saving at levels that will allow them to retire fully at age 65 at their current standard of living (reference). More than half of older Americans have less than $50,000 for retirement (reference). This is tragic for many. There is minimal to no teaching on personal finance in school, most advice is about budgeting and investing in the stock market, and despite all the information out there people still struggle. Financial advisors are often not true fiduciaries nor are they skilled or deeply educated in all areas of money and the pool of people entering the financial advisor career path is in crisis and shrinking.

Learning about money is often better done with people who have achieved financial goals who can act as mentors. And we believe there needs to be a Google Maps for money that helps people know what their route options are, how long it will take to arrive at financial goals, and make tradeoff decisions on where to go. We at FinJell plan to build this Google Maps for money to solve our own problems but hopefully the problems of many of you out there. If we’re successful, we hope that we’ll have helped many people become more financially secure and educated about their own money by providing the service and tools to make it easier to have more confidence in their financial future.

For now, we’ll start blogging about money and personal finance issues we’re tackling – this will be focused on the US market. We hope to do this in a way that adds value to all the existing information already out there. And hopefully the content here will not only be useful but will also give you some hints at what’s to come.

There probably isn’t anyone out there who doesn’t know that college costs keep going up. According to a recent US News & World Report annual survey, the average cost of tuition and fees for the 2021-2022 school year is $43,775 at private colleges, $28,238 for out-of-state students at public schools and $11,631 for state residents at public colleges. Unless you’re wealthy, these costs make many parents and future students wonder how they’ll be able to afford college prices. It seems like an article about the cost of college is written every year for as long as I can remember.

The classic advice is to use a 529 to save for your kids college education. Here, we’ll list out the set of options that are possible ways to save for college from the conventional to the less conventional.

529 Savings Plan

What is it?

529 savings plans are flexible, tax-advantaged accounts designed specifically for education savings for a student of any age. 529 plans let families set tax-deferred money aside for a child’s future education costs. Typically, a parent or grandparent opens the account and names a child or other loved one as the beneficiary. 529 plans were created to cover higher education expenses, but they can also be used to pay for some K-12 costs in certain states, with limitations that depend on the plan.

Every state offers its own 529 plan, and some private colleges and universities do too. Each plan is sponsored by an individual state, often in conjunction with a financial services company that manages the plan, although you don’t have to be a resident of a particular state to invest in its plan. 30+ states also offer residents additional state tax breaks on contributions (usually though not always for residents only).

A prepaid tuition 529 plan lets you prepay college tuition costs at today’s prices. It’s usually reserved for in-state public colleges and universities. While tuition and fees can be prepaid, room and board cannot. These plans aren’t guaranteed by the federal government, but some states back their plans and promise to provide funding if the program encounters financial issues. Not all colleges and universities participate, which could also limit where your child can attend school.

Savings Plans

A 529 savings plan lets you put after-tax dollars in investments like mutual funds and exchange traded funds (ETFs), and your money then grows tax-free. The earlier you open a 529 savings account, the longer the funds have to grow. These plans are usually sponsored by state governments and managed by financial services firms. Most states don’t require you to attend in-state public colleges using 529 money.

From what I can see, prepaid tuition plan makes sense only if you can guarantee your child will attend an in-state, public school, and only a few states currently offer prepaid 529 plans. Turns out, the history of 529 plans have their origin in prepaid tuition plans.

529 Savings Plans are the more popular and often better versions. They allow you to invest in stocks and bonds via preset investment menus. You can buy many yourself (direct-sold), and these are generally recommended because they’re cheaper. The remainder are sold by financial advisors; advisor-sold plans often have more investments but can be pricier because their expenses may include the cost of financial advice.

Direct-sold and advisor-sold college-savings plans come in two main varieties:

Age-based: The portfolio automatically shifts from risky, higher-earning securities (stocks) to less-risky investments (bonds) as your child nears college. This helps protect your money from being wiped out in a market downturn shortly before you’ll need to pay tuition bills.

With some age-based plans, you can fine-tune the stock and bond exposure by choosing an aggressive (more equity) or conservative (less equity) track. Others let you choose between an active or passive portfolio.

Static: The investment portfolio remains the same, or static, over time unless you manually adjust it.

A static portfolio lets you cook your own college-savings meal using ingredients from a preset investment menu: stock funds, bond funds, and balanced funds, which contain a set proportion of stocks and bonds.

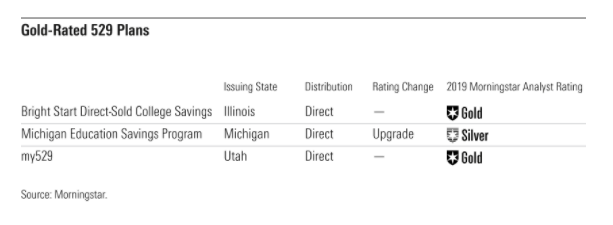

How Do I Find the Best 529 Plan?

529 plans are state-sponsored, but you can pick a plan from any state. These resources list out the top rated 529 plans:

Any earnings grow tax-deferred and qualified distributions are federal income tax free

No capital gains tax, ordinary income tax, or Medicare surtax

But each withdrawal from a 529 plan consists of both a contribution and an earnings portion

Gift and estate tax benefits1

Account owner may contribute up to $15,000 per year, per 529 account, without incurring federal gift tax. You can also “superfund” the account by making a contribution of up to $75,000 (or up to $150,000 for a married couple), then electing to treat the contribution as having been made over a five-calendar-year period for tax purposes (see IRS rules here)

Money contributed to a 529 plan account is generally considered removed from the owner’s estate

Contributions not limited by the income of the account owner

You can ask friends and family to make gifts to your child’s college savings account instead of new toys at birthdays and holidays. Those extra contributions can help boost your saving efforts

You can take withdrawals from a 529 plan to pay for qualified education expenses for more than just college-level education

Funds can be applied to elementary through high school level education or for beyond college (see Cons section for more details)2

Many families worry that saving for college will hurt their chances of receiving financial aid. But, because 529 savings plan assets are considered parental assets, they are factored into federal financial aid formulas at a maximum rate of about 5.6%. This means that only up to 5.6% of the 529 assets are included in the expected family contribution (EFC) that is calculated during the federal financial aid process. That’s far lower than the potential 20% rate that is assessed on student assets, such as assets in an UGMA/UTMA (custodial) account.

No required distributions

Beneficiary can be changed at any time

Account owner may transfer account at any time to another member of original beneficiary’s family3

Account owner maintains control over distribution of assets so owner can assure the money will be used for its intended purpose

Contributions considered revocable gifts

Owner controls the account; child is beneficiary

No age limit for the beneficiary

There are no time limits imposed on 529 plans

Beneficiary may keep contributing to a 529 plan throughout college or after graduation and use any leftover funds to repay student loans tax-free

529 Accounts have fees – though these fees have decreased over time

Person who creates the 529 account (account owner) must be 18 years or older, must be a U.S. citizen and must have a Social Security number or Tax ID

Plans are limited to one beneficiary at a time; families with multiple children may need more than one

The key to really get the most out of the investment in a 529 account is to start as early as possible. The later parents wait to open a 529, the less time for the money to grow. So, if you as parents are proactive enough to start making contributions when your children are babies, compounding will help you grow these funds significantly. But if you wait until your kids are teenagers, it’s not going to be that great of an investment.

Since this is an investment account, it does carry some risk, and there’s a chance you could lose money

For example: You cannot control the stock market’s performance and how that correlates to when your child needs college funds. It may be that your child enters college during the equivalent of 2008-2012 years when their 529 has lost half its value. Unfortunately, there’s really nothing you can do to control that and this is probably one of the biggest downsides of 529s

Although account owner chooses from portfolios with different exposure to equity and fixed income, the investment options are limited to mutual funds and exchange traded funds (ETFs)

For some families, their current investing strategy may outweigh the tax benefits of 529s, especially given the sub-par investment choices some 529s plans offer

If the investment earnings portion of the withdrawal is not used for qualified education expenses it will incur taxes and a 10% penalty. Those withdrawing funds for nonqualified expenses may also be required to pay back any state tax deduction they’ve received on contributions

Generally at the college or graduate level, funds from a 529 plan can be used for tuition, fees, books, supplies, approved study equipment, and room and board for a full-time student at an accredited institution

BUT if your child decides not to go to college, gets a full scholarship, or ends up attending a US military academy – there are options for these and other scenarios

A parent can transfer the 529 plan to a family member such as a sibling, first cousin or aunt, or even to themselves, to use for qualified education expenses

Although the owner may change the beneficiary, the eligible parties are limited, and risk-averse contributors should consider carefully in the beginning whether they believe there will be a qualified beneficiary, or if this option will even be desirable. Furthermore, changing the beneficiary does not help the original intended beneficiary. Maybe the child receives scholarships and grants. Should that child’s hard work be rewarded by passing their college fund down to a brother or sister?

$10,000 per year can be applied toward tuition expenses for elementary, middle, and high schools (private, public, or religious). Although the money may come from multiple 529 accounts, it will be aggregated on a per beneficiary basis, and any distribution amount in excess of $10,000 will be subject to income and a 10% federal penalty tax2

You can withdraw the amount of any scholarship awards from your 529 without penalty; federal and state income taxes on the earnings still apply

Can withdraw money anytime, with any earnings on nonqualified distributions subject to federal income taxes at the recipient’s rate as well as a 10% federal penalty

Distributions from 529s are made up of contributions and earnings in proportion to their levels in the account. That means that the portion of the withdrawal that is made up of your contributions would be tax-free and penalty-free but the earnings portion would be subject to taxes and the 10% penalty

529 beneficiaries can pay for qualified expenses related to apprenticeships with tax-free distributions. Funds from a 529 can be applied to expenses for fees, books, supplies, and equipment required for the participation of a designated beneficiary in an apprenticeship program registered and certified with the Secretary of Labor under Section 1 of the National Apprenticeship Act

Additionally, the law includes an aggregate lifetime limit of $10,000 in qualified student loan repayments per 529 plan beneficiary and $10,000 per each of the beneficiary’s siblings. Siblings may include a brother, sister, stepbrother or stepsister.

The SECURE Act made both changes retroactive, so any 529 distributions for apprenticeships or student loans made after December 31, 2018, are tax-free under the new law

1. In order for an accelerated transfer to a 529 plan (for a given beneficiary) of $75,000 (or $150,000 combined for spouses who gift split) to result in no federal transfer tax and no use of any portion of the applicable federal transfer tax exemption and/or credit amounts, no further annual exclusion gifts and/or generation-skipping transfers to the same beneficiary may be made over the five-year period, and the transfer must be reported as a series of five equal annual transfers on Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return. If the donor fails to survive the five-year period, a portion of the transferred amount will be included in the donor’s estate for estate tax purposes. Reference here

2. The Tax Cuts and Jobs Act of 2017, which went into effect on Jan. 1, 2018, expanded the use of 529 plans to include paying for private school tuition for kindergarten through 12th grade, up to $10,000 per year

3. For 529 accounts only, the new beneficiary must have one of the following relationships to the original beneficiary: 1) a son or daughter; 2) stepson or stepdaughter; 3) brother, sister, stepbrother, or stepsister; 4) father or mother or an ancestor of either; 5) stepfather or stepmother; 6) first cousin; 7) son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law; or 8) son or daughter of a brother or sister. The spouse of a family member (except a first cousin’s spouse) is also considered a family member. However, if the new beneficiary is a member of a younger generation than the previous beneficiary, a federal generation-skipping tax may apply. The tax will apply in the year in which the money is distributed from an account. Reference here

Custodial Account (Uniform Gifts to Minors Act [UGMA]/Uniform Transfers to Minors Act [UTMA] account)

What is it?

The Uniform Gift to Minors Act (UGMA) and Uniform Transfers to Minors Act (UTMA) are custodial accounts that allow you to invest for a college education or any other expense that benefits the minor. Funds in the account are considered an irrevocable gift that becomes the minor’s assets once they reach age of termination.

Distributions must be used for minor. Account owner controls the account until it is transferred to the minor at the age of termination.

Before the introduction of state-run 529 college savings plans, many parents invested for their children’s education and other major financial goals through UTMA or UGMA custodial accounts. When states began rolling out 529 college savings plans in the 1980s and ’90s, UGMA and UTMA accounts lost much of their appeal for college savers. The new 529 plans offered a number of tax advantages that UGMAs and UTMAs did not, including state tax breaks for contributions in many states and no federal taxes on earnings or withdrawals as long as the money in the plan was used for qualified educational expenses. UGMAs and UTMAs still exist, but people who use them today are likely to have goals other than paying for college in mind

If your primary goal is to invest for education, 529 plans offer the greatest tax advantages, control and flexibility. Custodial accounts can be good options to transfer wealth for just about anything else. If you want to make a contribution but aren’t sure if it will be used for education, the safest bet would be to put it in a custodial account. You or the beneficiary can move funds from a custodial account to a 529, but you can’t do the opposite without adverse income tax consequences

Pros:

No contribution limit, but gift taxes may apply for contributions over $15,000 annually ($30,000 per couple)

Can be funded with cash or securities

Anyone can contribute on behalf of the minor

Assets must be used for the benefit of the child, but can include non-college expenses

Withdrawals can be made at any time

Contributions not limited by the income of the account owner

Custodial accounts provide much more flexibility: They can be funded with any combination of cash and investments — normally, stocks, bonds, mutual funds, and so forth — although UTMAs also allow contributions of real estate, art and patents authorized by the account’s owner, or custodian, who is most commonly a parent or guardian of the minor for whom the account was set up

Cons:

Account is considered asset of the child (beneficiary) so it has higher weighting in financial aid eligibility formulas

UTMA or UGMA, is more likely to reduce your aid eligibility than money held in a parent’s name, as is the case for 529 accounts. Specifically, when the Free Application for Federal Student Aid (FAFSA) determines your expected family contribution toward college, it counts 20% of the student’s assets but no more than 5.64% of the parents’ assets

With a UTMA or UGMA custodial account, parents or others who set up the account decide how to invest the assets and how distributions are used — for school expenses or anything else that benefits the child. But when kids reach the age of majority (typically 18 or 21, depending on the state), they gain control and can spend the money however they like

UGMAs and UTMAs have fewer tax advantages than 529 plans

Generally, the first $1,100 of annual unearned income is tax-free, and the next $1,100 is taxed at the child’s tax rate. Unearned income above $2,200 is taxed at the rates for the child’s parents which may be higher than the child’s rate

Beneficiary cannot be changed

Beneficiary must be under 18 or 21, depending on state

Vermont and South Carolina do not support UTMA accounts

Coverdell Education Savings Accounts (ESAs) are tax-advantaged vehicles designed to help families save for elementary, secondary and college expenses. They operate similarly to 529 savings plans, but they have limits while also offering some additional unique benefits.

The two biggest limitations of the Coverdell ESA are: (1) that you’re only able to contribute $2,000 per year for each beneficiary, and only until they turn 18 and (2) you cannot contribute if Adjusted Gross Income is over $110,000 (for a single filer) or $220,000 (for a joint filer).

Coverdell ESAs have been around since 1998 – originally known as the Education IRA and later renamed after Senator Paul Coverdell (who sponsored the legislation that introduced them). The Economic Growth and Tax Relief Reconciliation Act of 2001 enhanced the benefits of using the Coverdell ESA, including:

Increasing the annual contribution limits from $500 to $2000 per beneficiary

Offering tax-free withdrawals for K-12 expenses

Allowing families who use Coverdell ESAs to claim other education tax benefits, as long as there is no “double-dipping”

These benefits were set to expire the end of 2012, which many feared would cause the Coverdell ESA to become obsolete. However, the American Taxpayer Relief Act of 2012 made the changes permanent, keeping the Coverdell ESA alive and another option to the 529 college savings plan.

You can contribute to both a 529 plan and an ESA for the same beneficiary if you wish. This was not permitted prior to 2002

Pros:

Distributions are federal income tax-free if used for the appropriate education expenses covered in any year to the extent that the beneficiary incurs qualified education expenses (QEE). If the beneficiary withdraws more than the amount of QEE, then the earnings portion of that excess is subject to income tax and an additional 10% penalty tax.

Both Coverdell ESAs and 529 plans can be used to pay for qualified higher education expenses, as defined by the Internal Revenue Service. But the rules differ regarding K-12 expenses. Tax free withdrawals from 529 plans are limited to K-12 tuition, while Coverdell ESAs can be used to pay for qualified elementary and secondary expenses

Each year, after a family takes the $10,000 maximum 529 plan distribution to pay for K-12 tuition, they have the option of withdrawing an additional $2,000 from the student’s Coverdell ESA to pay for other qualified expenses. (Just remember not to double-dip if you claim the American Opportunity Tax Credit or Lifetime Learning Credit)

Any earnings grow tax-deferred

Low impact on financial aid

Account is considered asset of the owner, not the child (beneficiary).

Lower weighting in financial aid eligibility formulas

An advantage of the Coverdell ESA over a 529 plan is the ability to self-direct investments. With a 529 plan, families are limited to investing in the investment portfolios offered by each plan

Similar to an IRA, with a Coverdell ESA parents will have greater flexibility when it comes to selecting investments, and will be able to choose from individual stocks, ETFs, mutual funds and even real estate

Account owner may transfer account to another family member (beneficiary)

You may take a rollover distribution from an existing ESA without triggering tax or penalty if you deposit the funds within 60 days into a different ESA for the same beneficiary or for any other qualifying member of the family. This 60-day rollover may be accomplished only once in a 12-month period

Can move the funds from a child’s ESA into a 529 plan tax-free to the extent that contributions are made to the 529 account for the same beneficiary in the same taxable year

Cons:

May only be used for education (college or K–12) expenses. Non-education uses will incur a penalty

Can withdraw money only for the benefit of the child

Beneficiary must be under 18

The ESA must be fully withdrawn by the time the beneficiary reaches age 30. If it is not, the remaining amount will be paid out within 30 days subject to tax on the earnings and the additional 10% penalty tax

Coverdell ESA phases out for parents with modified adjusted gross incomes between $190,000 and $220,000 ($95,000-$110,000 for single filers)

Unlike 529 plans, Coverdell ESAs are not operated or administered by the states, so there are no state tax benefits available

Coverdell ESA operates more like a custodial account, where the funds are the property of the beneficiary and cannot be revoked. With a 529 plan, the account owner, not the beneficiary, retains control of the assets over the life of the account

Funds in the account must be spent by the time the student turns 30, and at that time, any funds not withdrawn within 30 days may be subject to taxes and penalty

To avoid this, you can change the beneficiary on the account to another qualifying family member or roll the balance in to a 529 plan

Roth IRAs were created to encourage people to save for retirement. A Roth IRA is an individual retirement account that offers tax-free growth and tax-free withdrawals in retirement. Roth IRA rules dictate that as long as you’ve owned your account for 5 years and you’re age 59½ or older, you can withdraw your money when you want to and you won’t owe any federal taxes.

Unlike other retirement accounts, you can always withdraw the Roth IRA money you have contributed, any time, free of taxes and penalties.

Note the emphasis on “contributed” there. If you withdraw the investment earnings in your Roth account before age 59½, you’ll likely owe income taxes and a 10% penalty on the money you take out of the account.

There are some exceptions: If you take out Roth money to pay for qualified college costs, then you won’t owe the 10% penalty. You will, however, owe taxes on any investment earnings you withdraw (unless you’re over age 59½ and have owned the account for five years or more).

Financial aid is a bit tricky when comparing a 529 plan to a Roth IRA. Applicants include the value of a 529 plan in parental assets, if the plan is owned by a dependent student or his or her custodial parent(s), on the Free Application for Federal Student Aid (FAFSA), but not the value of a Roth IRA. Assets in a plan owned by others such as grandparents or another relative are not included on the FAFSA. Distributions from a plan owned by a dependent student or his or her custodial parent(s) are not included in income on the FAFSA. However, any money distributed from a plan owned by others such as grandparents or another relative and distributions from a Roth IRA in the prior year are included as untaxed income on the FAFSA. According to savingforcollege.com, income has a greater effect on financial aid than does the amount of parental assets. Though this may indicate one advantage for the 529 plan, parents can just wait to use Roth IRA distribution to pay for college after the student has filled out the FAFSA for the second year of college

For those parents with incomes beyond a certain level, the income may preclude them from contributing to a Roth IRA in the conventional manner. But backdoor and mega backdoor Roth options may still be available for these higher income level parents (see below – subject to potential 2021 legislation changes)

It can be difficult to choose between a 529 plan and a Roth IRA. But there’s nothing that says you can’t fund both, provided you’re financially able to do so. This can be a good strategy.

Pros:

Contributions and earnings grow tax free

For 2021 and 2020, you can contribute $6,000, or $7,000 if you’re age 50 or older. That means that over the course of 18 years, you could add up to $108,000, or $216,000 if you and your spouse both contribute to an IRA

Contributions (but not earnings) can be withdrawn at any time—income tax and penalty free with no required minimum distributions

Withdrawals are not taxed as earnings until the entire principal balance is used up

Once you reach 59½ and it’s been at least 5 years since you first contributed to a Roth, all money can be withdrawn tax and penalty free – thus, these withdrawals can be used to help with children and grandchildren’s college expenses

Clearly, the real magic of the Roth IRA happens if you waited until later in life to have kids or you’re saving for grandkids

If you withdraw earnings from a Roth IRA before you’re 59½ (or even if you are 59½ or older but you haven’t held the account for five years including conversions), you will pay taxes at your ordinary income tax rate and you will pay a 10% early withdrawal penalty

Qualified education expenses are an exception to the early withdrawal penalty. If you use a Roth IRA withdrawal for qualified education expenses, you will avoid the 10% penalty, but you will still pay income tax on the earnings portion

Value of Roth IRA is not included on the FAFSA used for financial aid consideration (but withdrawals do impact financial aid, see Cons section for details)

The rest of the Roth money not used for college expenses can remain in the Roth to fund your retirement

Roth IRA assets, as well as other qualified retirement accounts such as traditional IRAs or 401(k)s, are not counted at all in determining the expected family contribution that determines how much financial aid you are eligible to receive (a higher expected family contribution means less financial aid; the expected family contribution is calculated using information reported on the Free Application for Federal Student Aid)

Roth IRA is one of the most effective estate planning tools you can use so if there are unused funds these funds can benefit your heirs

Roth owners also appear to have a significant advantage when needing to change the beneficiary when compared to 529 accounts

Cons:

Roth IRAs do have income limits that constrains who can fund Roth IRAs and by how much

If you’re single, your contribution limits begin to phase out if you make $125,000 and above for 2021. If you are single and make $140,000 or above you are ineligible for a Roth IRA

If you’re married making $198,000 and above your contribution limits begin to phase-out, and couples who make $208,000 and above are ineligible

BUT there are currently ways around the income limits to contribute more to Roth IRAs (sadly may change in 2022)

The annual contribution is low, compared to what you can contribute to a 529

There’s no state income tax deduction for Roth contributions

If you use money from a Roth to pay for college, it will affect your expected family contribution two years after you use it. That’s because eventually the entire withdrawal shows up as income on the FAFSA form and counts at a 20%-50% rate–even the tax-free return of contributions, which shows up as untaxed income

To minimize the impact, don’t use a Roth IRA distribution to pay for college until the student has filled out the FAFSA for the second year of college

Giving away Roth money cuts retirement funds

But this consideration matters most to people who have this Roth as their primary retirement source. In this case, this also means Roth contributor may need to consider carefully whether the Roth contribution limits present an unacceptable trade-off

Many people use real estate to help pay for their kids future college education. There are 4 types of approaches to this:

Approach 1:

You acquire a property and earmark it specifically for the purpose of funding college tuition. This property is part of your real estate portfolio, but it doesn’t contribute to any other financial goals except funding college tuition

Buy a property

Sell or refinance the property when it comes time to pay for college

Use the proceeds to pay for your child’s college tuition – or whatever future he/she wants

Of course, this strategy is not going to work for just anyone who buys a piece of real estate. It works best if the property cash flows or breaks even. The best way to approach it is to follow the “BRRRR Strategy” (buy-rehab-rent-refinance-repeat) [see BiggerPockets] which is: buy right so you can add value, rehab property to make it “tenant proof” in terms of what materials to use etc and to attract the best tenants, make sure the property is always rented and maintained well (can use property manager), and then you can refinance/sell when needed. If you buy right, then the tenants are basically paying for your property and you can apply excess rental cash flow to accelerate debt pay down or invest these excess cash flow funds into a 529 to get both the benefits of real estate and the 529 plan!

One additional key part of this approach is that your child can learn about real estate and finance by owning and being responsible to take care of the property over the years and particularly during college and beyond.

Approach 2:

If you don’t want to set aside a property specifically for saving for college and you plan to build a substantial real estate portfolio, your strategy can be to fund college tuition from your balance sheet. Here, you look at tuition cost as an annual expense funded from your income statement.

For instance, the cost of tuition for Year 1 is $46,124, Year 2 is $48,430, Year 3 is $50,851, and Year 4 is $53,394. You build a portfolio that produces the required income to cover the tuition expense in each of the four college years. The principal difference between this and approach 1? After you fund college, you still own the assets.